New Measurement proposals - IPSASB EDs

Tier 1 and Tier 2

The International Public Sector Accounting Standards Board (IPSASB) has published four exposure drafts (EDs) dealing with measurement of assets and liabilities.

- ED 76 Conceptual Framework Update: Chapter 7, Measurement of Assets and Liabilities in Financial Statements

- ED 77 Measurement

- ED 78 Property, Plant and Equipment

- ED 79 Non-current Assets Held for Sale and Discontinued Operations

Here we provide a detailed summary of each ED and why you might be interested in them.

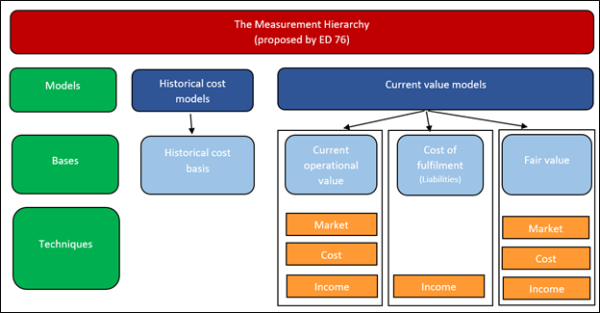

ED 76 updates Chapter 7 of the IPSASB Conceptual Framework. It proposes a new approach – current operational value – to measuring assets held for their operational capacity. It would also remove some of the measurement approaches currently mentioned in Chapter 7, but which have not been used in standards.

ED 77 proposes a new IPSAS which explains how to apply historical cost, fair value (aligned with IFRS 13 Fair Value Measurement), current operational value (the new approach) and cost of fulfilment when measuring assets and liabilities.

ED 78 proposes to update IPSAS 17 Property, Plant and Equipment, including changing the requirements for revalued assets. Some revalued assets would be measured using fair value (updated to be aligned with fair value as per IFRS 13) and some using current operational value (the new approach). These proposals would have the most impact on assets used in delivering goods and services that are currently measured using depreciated replacement cost – such assets would most likely be measured using current operational value. ED 78 also proposes some additional guidance on heritage and infrastructure assets.

ED 79 proposes a new IPSAS based on IFRS 5 Non-current Assets Held for Sale and Discontinued Operations. Although this would fill a gap in IPSAS, we already have a PBE Standard based on IFRS 5 in New Zealand.

The proposals in the EDs are relevant for Tier 1 and Tier 2 public benefit entities (PBEs)—both not-for-profit and public sector entities. Once the IPSASB completes these projects, the NZASB will consider if equivalent changes should be made to PBE Standards. We therefore encourage all Tier 1 and Tier 2 PBEs to consider the proposals and provide feedback.

Who should read these EDs?

If you:

- Refer to Chapter 7 in the PBE Conceptual Framework, have a look at ED 76.

- Currently measure assets at fair value under PBE Standards, use the guidance on depreciated replacement cost in PBE IPSAS 17 Property, Plant and Equipment, or deal with assets with restrictions, have a look at ED 77 and ED 78.

- Currently apply PBE Standards to heritage or infrastructure assets, have a look at ED 78.

- Regularly engage valuers to value specialised assets, have a look at ED 77 and ED 78.

Webinar - 8 July 2021

This gave an overview of the proposals and highlighted areas of interest.

Accessing the consultation documents

|

|

Exposure Draft |

At-a-Glance |

|---|---|---|

|

ED 76 |

|

|

|

ED 77 |

|

|

|

ED 78 |

|

|

|

ED 79 |

|

|

Commenting on the proposals

Submissions closed on 2 September 2021