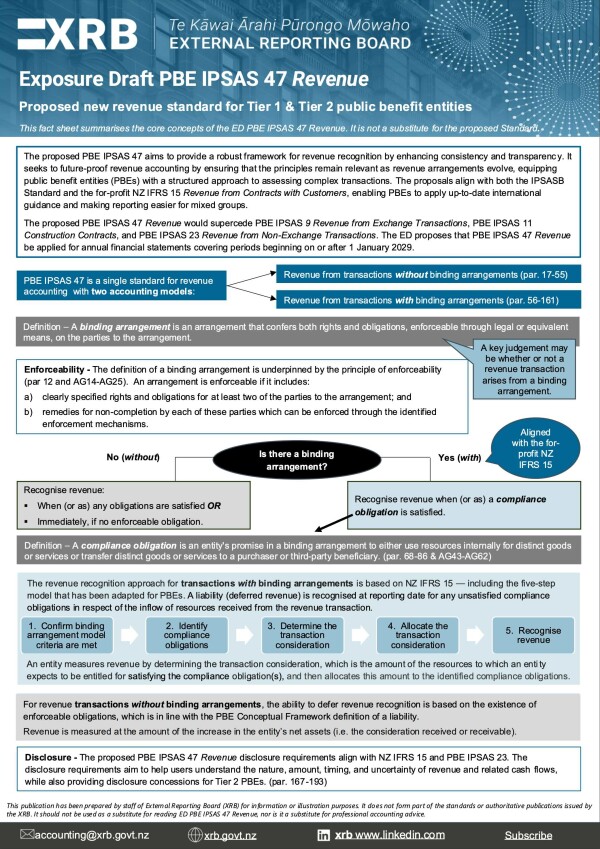

Proposed accounting standard for revenue – ED PBE IPSAS 47 Revenue

Exposure Draft (ED) PBE IPSAS 47 Revenue proposes new accounting requirements for revenue transactions. The proposed standard aims to provide a robust framework for revenue recognition by enhancing consistency and transparency.

The proposed PBE IPSAS 47 Revenue would supersede PBE IPSAS 9 Revenue from Exchange Transactions, PBE IPSAS 11 Construction Contracts, and PBE IPSAS 23 Revenue from Non-Exchange Transactions.

Consultation closed on 1 December 2025. Submissions received are listed on the main consultation page here.

About ED PBE IPSAS 47 Revenue

|

ED PBE IPSAS 47 is a single source for revenue accounting guidance for Tier 1 and Tier 2 public benefit entities (PBE). The proposals present two accounting models based on the existence of a binding arrangement. This new standard provides focused guidance to help entities apply the principles to account for all PBE revenue transactions. The ED proposes that PBE IPSAS 47 Revenue be applied for annual financial statements covering periods beginning on or after 1 January 2029. |

Our exposure draft and accompanying consultation document detail the proposals

|

|

View our proposals for transfer expense accounting here.

Educational guidance and support

One of the key benefits of this proposed standard is the inclusion of clear guidance, supported by 56 illustrative examples, aimed at enhancing consistency in accounting for revenue transactions.

We have created a fact sheet and short webcasts summarising key concepts included in the proposed ED.

|

|

Events

- Need to Know - Accounting update for Tier 1 and Tier 2 public sector entities. You can view the recording here and download the event slides here.

- Need to Know - Accounting update for Tier 1 and Tier 2 not-for-profit entities. You can view the recording here and download the event slides here.