IFRS Interpretations Committee

The main activity of the IFRS Interpretations Committee (the Committee) is responding to questions about the application of IFRS Standards. The Committee response may include developing explanatory material or recommending that the International Accounting Standards Board (IASB) amend the existing IFRS Standards.

It is important to understand the status of decisions made by the Committee because they may impact how you go about preparing your financial statements in compliance with NZ IFRS.

|

Although agenda decisions are specifically developed with for-profit entities in mind, public sector or NFP public benefit entity's (PBEs) applying Tier 1 or Tier 2 PBE Standards may also consider applicable explanatory material in IFRS Interpretations Committee agenda decisions when developing and applying accounting policies in accordance with PBE IPSAS 3. |

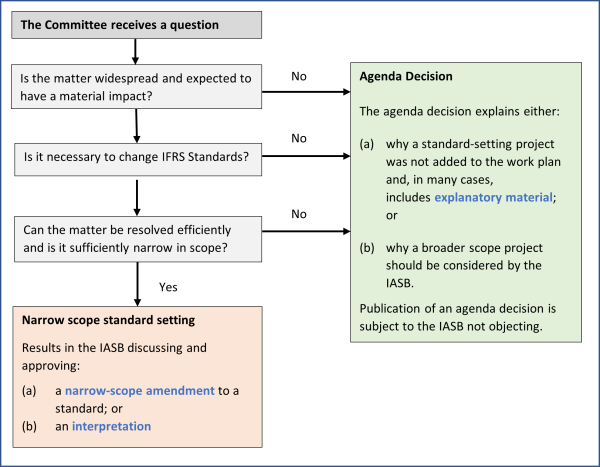

Overview of IFRS Interpretations Committee process and status of agenda decisions

The diagram below provides a summary of the Committee process when responding to questions received.

Agenda decisions – including any explanatory material within them – cannot add or change requirements in IFRS Standards. Instead, the explanatory material explains how the applicable principles and requirements in IFRS Standards apply to the transaction or fact pattern described in the agenda decision.

When preparing NZ IFRS compliant financial statements, consideration should be given to applicable explanatory material in agenda decisions.

Recent IFRS Interpretations Committee activities

The IFRS Interpretations Committee publishes tentative agenda decisions for comment before finalising those decisions. Please click on the button below for information on recent tentative and final agenda decisions.

Accessing all IFRS Interpretations Committee agenda decisions

You can search agenda decisions by date and by standard: