XRB Position Statement on EER

8 March 2019

The External Reporting Board (XRB) strongly supports the reporting of EER information by entities within their annual report to the extent that the information is relevant to the intended users of annual reports.

The XRB considers that other types of, or more detailed, EER information, which may be demanded by other stakeholders, may be better located outside of the annual report.

The purpose of this Position Statement is to state the XRB’s position on the reporting of EER information by entities within their annual report. This Position Statement is not intended to provide guidance for the preparation and presentation of EER information.

Extended External Reporting (EER) is an umbrella term adopted by the XRB to refer to broader and more detailed types of reporting beyond the types of information presented in an entity’s statutory financial statements. EER can include reporting information on an entity’s governance, business model, risks, opportunities, prospects (including forward-looking financial information), strategies and economic, environmental, social and cultural impacts.

EER encapsulates integrated reporting, sustainability reporting, non-financial reporting, pre-financial reporting, management discussion and analysis, management commentary, ESG reporting (environmental, social and governance), corporate responsibility reporting, community and environmental reporting and more.

The XRB has a significant interest in EER, given its role as an independent Crown Entity responsible for financial reporting strategy and the development and issuance of accounting and auditing and assurance standards in New Zealand.

The XRB has observed growing demand from stakeholders, supported by research, for entities to provide:

- increased transparency on material risks (including ESG risks) and strategies for managing those risks;

- forward-looking information about an entity’s long-term sustainability;

- information about an entity’s key resources and relationships; and

- greater visibility around corporate citizenship.

The XRB acknowledges the demand for EER by stakeholders and is strongly supportive of entities presenting EER.

However, when considering what EER information should be included in annual reports, the XRB considers that a distinction needs to be drawn between EER relevant to the intended users (audience) of annual reports and EER provided for other purposes, such as public policy purposes.

Drawing this distinction helps to ensure that EER enhances, rather than impairs, the effective communication of relevant information to the intended users of annual reports.

In issuing its standards, the XRB focuses on users’ needs for information in general purpose financial reports (GPFR).

The primary users of GPFR of for-profit entities [1] are existing and potential investors, lenders and other creditors. The primary users of GPFR of public benefit entities [2] are resource providers (e.g. taxpayers, ratepayers, donors and grantors), service recipients and their representatives. The XRB considers that the primary users of GPFR and the intended users (audience) of annual reports are the same.

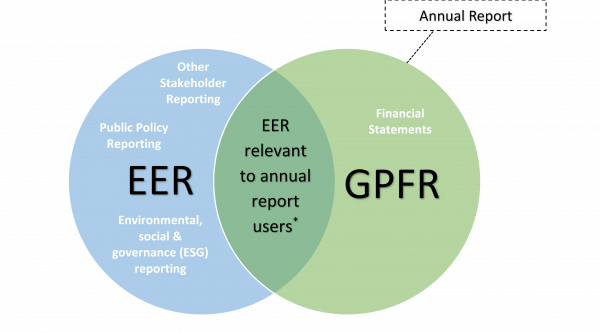

EER information that is relevant to the primary users of GPFR may also be relevant to a wider group of stakeholders, such as NGOs, regulators, consumers and employees. The relationship between EER information that is relevant to the intended users of annual reports and EER information that is relevant to a wider group of stakeholders is illustrated in the diagram below.

* Determining EER information that is relevant to the intended users of the annual report can require significant judgement. The XRB intends to promote resources to assist entities in making such judgements.

Where more detailed EER on a specific topic (for example, climate change [3]) is required for public policy purposes but is not relevant to users of the annual report, in order to avoid ‘information overload’ the XRB believes that such EER should be presented outside the annual report.

Information overload undermines the relevance and understandability of the annual report for its intended users. Equally, the XRB believes that detailed EER on a specific topic may be more visible/accessible to its intended audience if it is reported outside the annual report, for example, in a separate report to a regulator, prudential supervisor or government agency or presented on an entity’s website.

The XRB supports the continued innovation in EER and is committed to working collaboratively with key stakeholders, including policy makers and regulators, to help generate the right balance between policies, regulation and innovation.

In addition, the XRB is undertaking other activities relating to EER:

- Providing an EER navigational resource to help you make better-informed decisions when considering EER.

- Considering developing guidance on EER.

- Considering the assurance implications of EER.

Why undertake EER?

Find useful EER Resources