Making Materiality Judgements

Phase 2

|

We are consulting on an Exposure Draft issued by the International Public Sector Accounting Standards Board (IPSASB), which proposes guidance to help public sector entities in making materiality judgements when preparing financial statements. |

|

The proposals form Phase 2 of the IPSASB’s materiality project and aim to provide practical guidance to support consistent, entity‑specific judgements. If introduced in New Zealand, this guidance would support Tier 1 and Tier 2 public benefit entities (PBEs) in applying materiality in general purpose financial reporting.

Background: The IPSASB's project on materiality

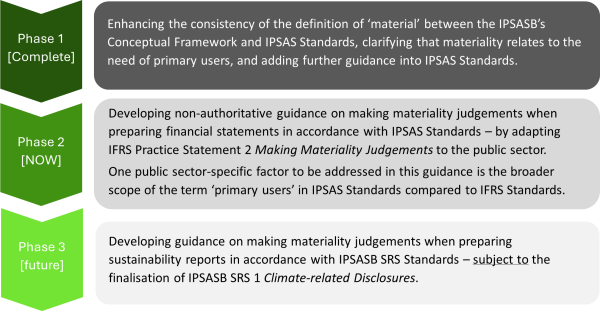

The IPSASB received feedback that public sector entities sometimes face difficulties in making materiality judgments when preparing general purposes financial reports. These difficulties can result in entities providing too much irrelevant information and/or not enough relevant information in their financial reports. The IPSASB commenced a project on materiality to address these difficulties.

The IPSASB’s project on materiality will have three phases, as shown below. The IPSASB is currently at Phase 2.

* Note the outcome of Phase 1 has not yet been adopted in NZ. For more information, see our Phase 1 consultation page.

Phase 2 proposals at a glance

The IPSASB Exposure Draft proposes non-authoritative guidance to support materiality judgements when preparing financial statements in accordance with IPSAS.

The IPSASB's proposed guidance is based on the IASB's Practice Statement 2 Making Materiality Judgements, with modifications for the public sector context and consistency with IPSASB literature.

The proposed guidance focuses on:

· Applying materiality in the public sector context - noting that the definition of 'material' in IPSAS 1 refers to the information needs of primary users for both accountability and decisions making purposes, and that primary users in the public sector comprise resource providers, service recipients and their representatives

· identifying material information, both qualitatively and quantitatively

· avoiding over‑disclosure and the obscuring of material information

· supporting consistent but entity‑specific judgements, recognising the diversity of public sector entities and users

Note: The proposed guidance in the Exposure Draft is based on the updated definition of 'material' in IPSAS 1, as updated by the IPSASB in 2024:

"Information is material if omitting, misstating or obscuring it could reasonably be expected to influence the discharge of accountability by the entity, or the decisions that primary users make based on the basis of the entity's general purpose financial statements prepared for that reporting period".

(The reference to obscuring information and the emphasis on primary users is not yet included in PBE IPSAS 1).

We want to hear from you

We welcome feedback on the proposals, including:

- whether the guidance is useful and practical for public sector entities

- whether it appropriately reflects public sector circumstances and user needs

- any implementation challenges, costs, or unintended consequences

Your feedback will inform our submission to the IPSASB. It will also inform future considerations on whether and how to update the XRB's non-authoritative materiality guidance relating to PBE Standards.

Read Exposure Draft 97 here

Read the IPSASB’s ‘at a glance’ summary here

Draft comment letter

|

We have also drafted a submission to the IPSASB that contains our preliminary views on IPSASB ED 97, including:

We would appreciate your consideration of the preliminary views outlined in the draft submission, including any comments on additional matters or detail that should be incorporated. |

|

How to provide feedback

Comments to the XRB are now closed. However, comments can still be made directly to the IPSASB until 28 August 2026.