Resources

The External Reporting Board (XRB) is proud to play its part in addressing climate change through the establishment of a climate-related disclosures framework for Aotearoa New Zealand. The XRB has created guidance and resources to support entities when applying Aotearoa New Zealand Climate Standards.

Previous consultation documents, exposure drafts and supporting documents can be found on our consultation page.

Guidance

|

All Sector Staff Guidance for NZ CS To support entities required to prepare disclosures in accordance with NZ CS. It illustrates how an entity may approach the required disclosures. Download the PDF version.

|

|

|

|

MIS Manager Staff Guidance for NZ CS To support managers of registered investment schemes (MIS Managers) required to prepare disclosures in accordance with NZ CS. It illustrates how an MIS Manager might approach the required disclosures. Download the PDF version.

|

|

Transition planning disclosures guidance This guidance provides further, detailed guidance relating to transition planning disclosures to supplement the Guidance for All Sectors. It covers all elements relating to transition planning disclsoures. Download the PDF version.

|

|

|

Transition planning - Questions to get started What is transition planning, where to start, and some common misconceptions. Download the PDF version.

|

|

Principles and general requirements of NZ CS 3 walkthrough webcast Watch a short webcast which outlines the principles and general requirements in NZ CS 3 which are an important part of applying the Climate Standards. |

|

|

Entity-level Scenario Analysis Staff Guidance How to develop useful, plausible, consistent, and challenging scenarios for climate-related disclosures under NZ CS 1. Download the PDF version.

|

|

Staff are currently working on guidance relating to anticipated financial impacts (AFIs). This guidance is due to be published in mid-2026.

|

Staff guidance: Anticipated financial impacts

|

|

|

NZ CS and AASB S2 interoperability overview and tool This overview and tool describes the alignment of disclosure requirements and information that an entity starting with each set of standards needs to know to enable compliance with both sets of standards, ensuring interoperability between them.

|

|

Climate transition planning: Overview This guidance is to provide an overview of what climate transition planning is and how it can help organisations transform deep uncertainties into an actionable long-term strategy. Download the pdf version below.

|

|

|

Climate transition planning: Executives guide Transition planning impacts across the entire organisation and the future direction of the business. Executives have a critical role to play in terms of leadership, strategy, and execution. This guide is executives' "need to know" about transition planning. Download the pdf version below.

|

|

Transition planning: A guide for directors This guidance is a introductory reference for directors of Climate Reporting Entities (CREs) as they commence transition planning but can also be used to support transition planning by the broader governance community. Download the pdf version below.

|

|

|

Transition planning: A guide for staff This guide is for staff involved in coordinating or leading the transition planning process in their organisation. It covers the thinking and related business processes to develop a transition plan, as well as the drafting of the transition plan itself. Download the pdf version below.

|

|

Navigating climate statements guide This joint FMA/XRB guide is an explanation of the information disclosed in climate statements. This guide highlights the importance of topics such as uncertainty, comparability and context when evaluating and judging the information they contain. Download the pdf version below. |

|

Climate-related Disclosures Regime: This joint FMA/XRB guide provides an overview of the Climate-related Disclosures regime including: the purpose of disclosing climate-related information; key legislative requirements; key considerations and context about the information in climate statements and the roles of the FMA, XRB and relevant government agencies. |

|

|

Climate-related matters in financial statements This guidance is intended to help Climate Reporting Entities understand the requirements in New Zealand accounting standards relating to climate-related matters in financial statements. Download the PDF version below.

|

|

Comparison Document: Aotearoa New Zealand Climate Standards and IFRS® Sustainability Disclosure Standards A staff comparison of requirements in Aotearoa New Zealand Climate Standards (NZ CS) with the International Sustainability Standards Board’s two sustainability disclosure standards. Download the PDF version below.

|

|

|

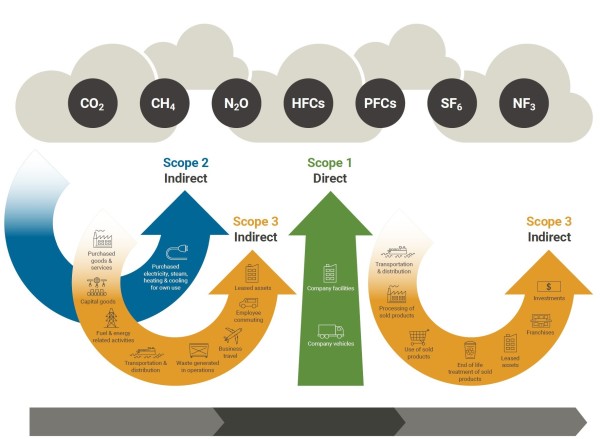

Getting started on measuring your emissions This document defines scope 1, 2 and 3 emissions sources and details the steps on measuring and disclosing them. Read more here, or download the PDF version below.

|

|

Director Preparation guide This guide is intended to provide directors with a quick reference for key things they need to know about Aotearoa Read more here, or download the PDF version below. |

|

|

GHG Assurance Reports - Explainer This guide is for readers of climate statements. It highlights what to look out for in the assurance reports that will accompany climate statements prepared by climate reporting entities. Download the PDF version.

|

|

Scenario analysis fact sheet The scenario analysis fact sheet clarifies the definition and purpose of scenario analysis for Aotearoa New Zealand Climate Standard 1: Climate-related Disclosures (NZ CS 1). Read more here, or download the PDF version below. |

|

|

Scenario analysis: Getting started at the sector level How to develop consistent and comparable sectoral scenarios for Climate-related Disclosures under NZ CS 1. Download the PDF version below. |

FAQs

Climate-related disclosures are mandatory for large listed companies (large meaning with a market capitalisation of more than $60 million); large registered banks, licensed insurers, credit unions, building societies, and managers of investment schemes (large meaning with more than $1 billion in assets). See Part 7A of the Financial Markets Conduct Act 2013 for more detail.

Some Crown financial institutions (via letters of expectation) are also expected to report.

The mandatory reporting regime commenced for the first accounting period for the climate reporting entity that began on or after 1 January 2023. For example:

- A reporting entity with a 31 December balance date (i.e., reporting period 1 January to 31 December) is required to prepare their first climate statement as part of their 31 December 2023 reporting.

- A reporting entity with a 30 June balance date (i.e. reporting period 1 July to 30 June) is required to prepare their first climate statement as part of their 30 June 2024 reporting.

The Financial Markets Authority (FMA) are responsible for monitoring, regulation and enforcement.

We continue to keep a close eye on international developments. This includes mandatory climate-related disclosure regimes in other jurisdictions such as Australia and the United States, as well as voluntary regimes such as the work coming out of the International Sustainability Standards Board (ISSB) and the Global Reporting Initiative (GRI).

It is a fast-evolving space and we will continue to monitor international developments. For a comparison between Aotearoa New Zealand Climate Standards and the ISSB's IFRS S2 Climate-related Disclosures, see here.

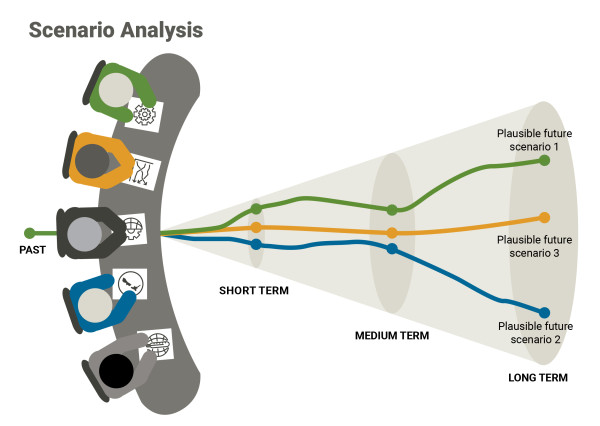

Scenario analysis is primarily a tool to enhance strategic thinking on climate-related risk and opportunity.

Climate-related scenarios are plausible, challenging descriptions of how the future may unfold. These descriptions are based on coherent and internally consistent sets of assumptions about the drivers of future physical and transition risk and opportunity (and the relationships between them).

Undergoing a scenario analysis is to an organisation what a wind tunnel is to a plane: This is about exploring how it could behave under challenging but plausible conditions it may face and how the aircraft can be improved.

The purpose of scenario analysis under NZ CS 1 is to help entities to explore the climate-related risks and opportunities they may face and the resilience of their business model and strategy.

This exploratory analysis must include, at a minimum, a 1.5°C climate-related scenario, a 3°C or greater climate-related scenario, and a third climate-related scenario. These scenarios should integrate elements of physical and transition risk and opportunity.

Entities are required to undertake their own scenario analysis at entity level as part of NZ CS 1, not sector level scenario analysis. However, sector specific scenarios will facilitate this process and reduce the overall resource required to undertake the analysis and will allow entities to focus on its specific risks and opportunities, business model and strategy.

The TCFD has published comprehensive guidance on the use of scenario analysis in disclosing climate-related risks and opportunities. Further information is also available in the External Reporting Board’s Guidance for All Sectors.

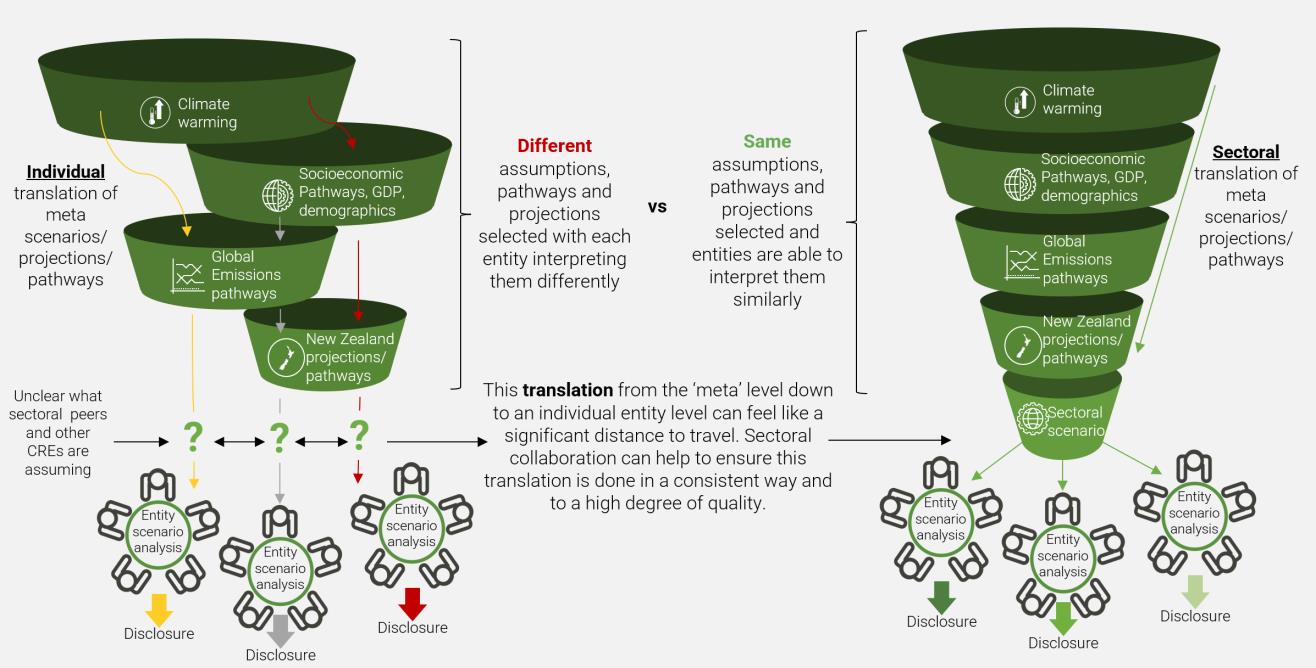

Sectors can develop climate-related scenarios. To be plausible and decision-relevant for Climate Reporting Entities (CREs), sectoral scenario analysis benefits from participation of the entire sector. The expertise, experience, and perspectives of the sector, in combination with insights and perspectives from outside the sector, provide the key ingredients for relevant and compelling scenarios.

Primary users, including investors, have indicated a strong desire for comparability in disclosures, which is one of the main drivers for the introduction of Aotearoa New Zealand’s mandatory regime. The challenge for CREs is to bridge the divide between the scales of analysis available globally and nationally, and what is relevant to them as an individual entity. Sectoral scenarios offer the most practical and flexible means of doing so. Although not a mandatory approach, sectoral collaboration is likely to provide greater comparability and lead to higher quality scenarios, while imposing fewer resource demands on CREs.

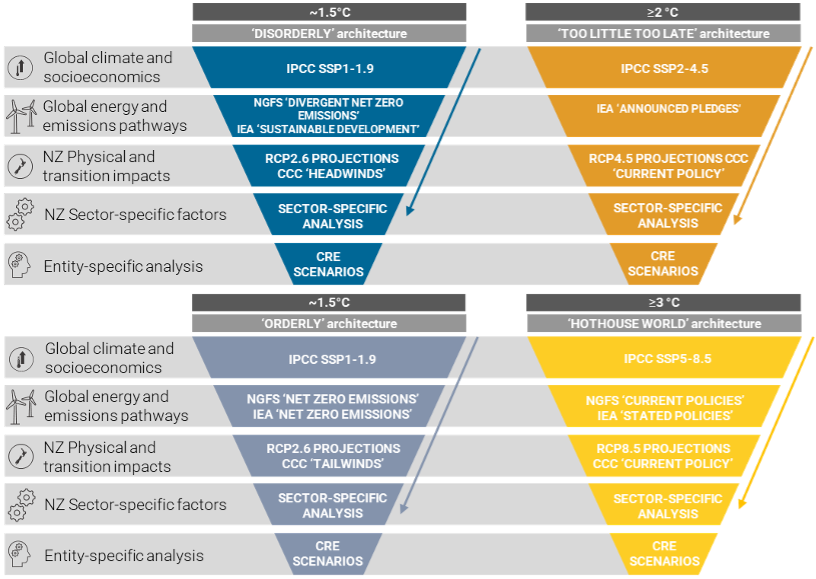

Figure 1: The role of sectoral scenarios in creating a shared scenario architecture for the use of CREs in New Zealand

In Appendix 1 of the Guidance on Getting Started on Scenario Analysis at the Sector Level, the XRB has developed guidance on broadly aligned sets of scenarios, pathways and projections that can form a shared architecture for sectoral scenarios. These are loosely based on the structure of the NGFS climate scenarios. This approach to envisioning futures which are differentiated by the scale of physical and transition risk they embody is gaining traction globally. Adopting it as the structure for sectoral scenarios in New Zealand will help to align sectors with global financial climate-related risk analysis practices. These cones provide high-level assumptions and building blocks which are plausible and broadly coherent, and can be used to paint a picture of the world an entity might find itself in.

In September 2020, the Government announced its intention to implement mandatory reporting on climate risks and tasked the XRB with developing reporting standards to support the new reporting regime.

In October 2021, the Financial Sector (Climate-related Disclosures and Other Matters) Amendment Act was passed. As a result, the XRB had a mandate to issue climate standards as part of a climate-related disclosures framework, and non-binding guidance on non-financial matters.

Under the climate-related disclosure framework, scope 1 and 2 GHG emissions do not pertain to MIS Managers. This is because Section 461O of the Financial Markets Conduct Act 2013 defines MIS Managers as climate reporting entities in respect of the scheme they manage. Therefore, no disclosures are required. Because there is no disclosure, there is no need for a related assurance engagement.

We recommend that MIS Managers include the following wording in their climate statements to clarify this point to their primary users:

“Note on emissions disclosures: scope 1 and 2 greenhouse gas emissions do not pertain to MIS Manager disclosures because S461O of the Financial Markets Conduct Act 2013 defines MIS Managers as climate reporting entities in respect of the scheme they manage, therefore no disclosures are required”.

If a MIS Manager chooses to make scope 1 and 2 GHG emissions disclosures, even if it says zero or nil scope 1 and 2 GHG emissions, it would need to obtain an assurance engagement over that disclosure.