Emissions are a prime driver of rising global temperatures and, as such, are a key focal point of policy, regulatory, market, and technology responses to limit climate change. As a result, climate reporting entities (CREs) with significant emissions are likely to be impacted more significantly by transition risk than other entities.

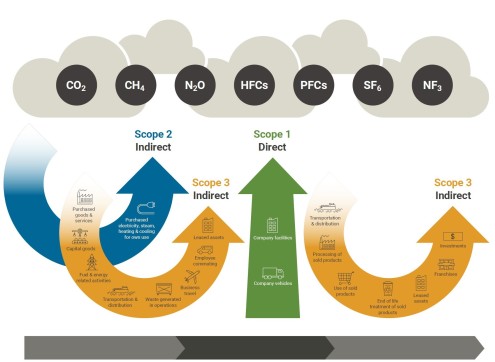

Figure 1: Greenhouse gas emissions: Scope 1, 2 or 3

GHG emission sources are either scope 1, scope 2 or scope 3 activities. Current or future constraints on emissions, either directly by emission restrictions or indirectly through carbon budgets, may impact entities financially.

Scope 1

Direct emissions from sources owned or controlled by the CRE (i.e., within the entity boundary). For example, emissions from combustion of fuel in vehicles owned or controlled by the CRE.

Scope 2

Indirect emissions from the generation of purchased energy (in the form of electricity, heat or steam) that the CRE uses.

Scope 3

Other indirect emissions occurring because of the activities of the CRE but generated from sources it does not own or control.

Purchased goods and services

Capital goods

Fuel and energy related activities

Upstream transportation and distribution

Waste generated in operations

Business travel

Employee commuting

Upstream leased assets

Downstream transportation and distribution

Processing of sold products

End of life treatment of sold products

Downstream leased assets

Franchises

Investments (financed emissions fall into this category)

To quantify and report GHG emissions a CRE will need data about its activities (e.g., quantities of fuel used). This is then converted to emissions using emission factors. The consolidated data forms the inventory and is reported in the GHG emissions report.

The importance of value chain emissions

Until recently, entities have focused their attention on emissions from their own operations. But increasingly entities understand the need to also account for GHG emissions along their value chains and product portfolios to comprehensively manage GHG-related risks and opportunities.

Value chain refers to all the upstream and downstream activities associated with the operations of the CRE, including the use of sold products by consumers and the end-of-life treatment of sold products after consumer use. Value chain emissions are generally where an entity’s greatest risks and opportunities lie.

Five steps to measure and disclose

Select the organisation boundary (including consolidation approach) and the measurement period. CRE boundaries are set in legislation (Part 7A of the Financial Markets Conduct Act 2013). Your measurement period should be in alignment with your financial reporting period. Most organisations in New Zealand use an operational control consolidation approach.

Set your operational boundary. Identify emissions associated with your operations, categorising them as direct and indirect emissions. Refer to the GHG Protocol Corporate Value Chain Standard for comprehensive guidance on value chain emissions.

Collect activity data on each emissions source within the boundaries for that period.

Multiply the activity data used by the appropriate emission factor in a spreadsheet. The Ministry for the Environment publishes emission factors for common emissions sources.

Produce a GHG emissions report and get assurance. Prepare a GHG emissions report in compliance with your chosen standards (e.g., GHG Protocol or ISO 14064). Assurance provides an independent assessment of the reliability (considering completeness and accuracy) of a GHG emissions report.

The GHG Protocol provides comprehensive guidance

The GHG Protocolprovides comprehensive guidance on the core issues of GHG monitoring and reporting at an organisational level, including:

The GHG Protocol’s standards and guidance are free to download.

ISO 14064-1:2018is another commonly used standard for measuring and reporting GHG emissions. It is closely based on the GHG Protocol but is shorter and more direct. It must be purchased.

Glossary

Activity data: A quantitative measure of a level of activity that results in GHG emissions e.g., quantity of fuel used. Activity data is multiplied by an emissions factor to derive the GHG emissions associated with a process or an operation.

Emission factor: A factor allowing GHG emissions to be estimated from a unit of available activity data, e.g., litres of fuel consumed, and absolute GHG emissions.

Inventory: A quantified list of an entity’s GHG emissions and sources.

GHG emissions report: A GHG emissions report gives context to the GHG inventory by including information about the entity, comparing annual inventories, discussing significant changes to emissions, listing excluded emissions, and stating the methods and references for the calculations.